GRA

Well-known member

WetEV said:90% of vehicles sold in Norway are EVs. I'd expect you to be in the last 10% here, based on your use case. Looking ahead, we are a decade behind Norway, so you have a decade or a bit more to whine about why you don't want an electric. And I'd expect used ICEs for another decade or two would be an option.GRA said:How long does it take you to decide that hitting your head with a hammer hurts and is unacceptable, before you stop?WetEV said:Once you have an EV, your opinions about what home wiring and OBCs might be more useful. Experience can teach. My opinions about horses are worthless, as I have never have maintained a horse. I have little experience with horses.

Why don't we pause this discussion until fuel cell car sales collapse as manufacturers give up, or *EV sales exceed 50%?

If I lived in Norway, a country ~10% smaller than California, had no need to travel outside it, and had the kind of bribes and infrastructure available to them that we don't have here, I'd have been one of the first 10% to get a BEV. As it is, I expect I'll be somewhere in the 50% range here. As to how long I have to wait, I've already been waiting more than a decade for a ZEV to become available that will allow me to resume taking out of state trips, and I'm damned tired of waiting.

I'm perfectly willing to put this particular round of the argument on hold, although we both know it will burble up again in a month or so. FCEV passenger cars will or won't become a viable consumer option depending on the speed and amount of improvement of BEVs and their infrastructure, vis a vis the rate of FCEVs likewise. FCEV or maybe even H2/ICE heavy transport, OTOH, is definitely going to be a major part of future ZEVs.

WetEV said:GRA said:Again, you assume that the majority of the public shares your perceptions and priorities, and that H2 infrastructure can never be built. Well, in the case DCFC for long-distance trips, barring a corporation getting caught being very naughty such (non-Tesla) infrastructure still wouldn't exist here, and you couldn't do any such trips in your e-Tron, unless you make the whole trip a BEV adventure like Tony Williams' BC2BC.

Note that Tony's BC2BC got way too easy, and was no longer an adventure. Last one was in 2014. Tesla cars got too easy first, but it is now too easy for everyone.

https://abetterrouteplanner.com/?plan_uuid=61b2bdda-3481-43de-9bec-cce196562c22

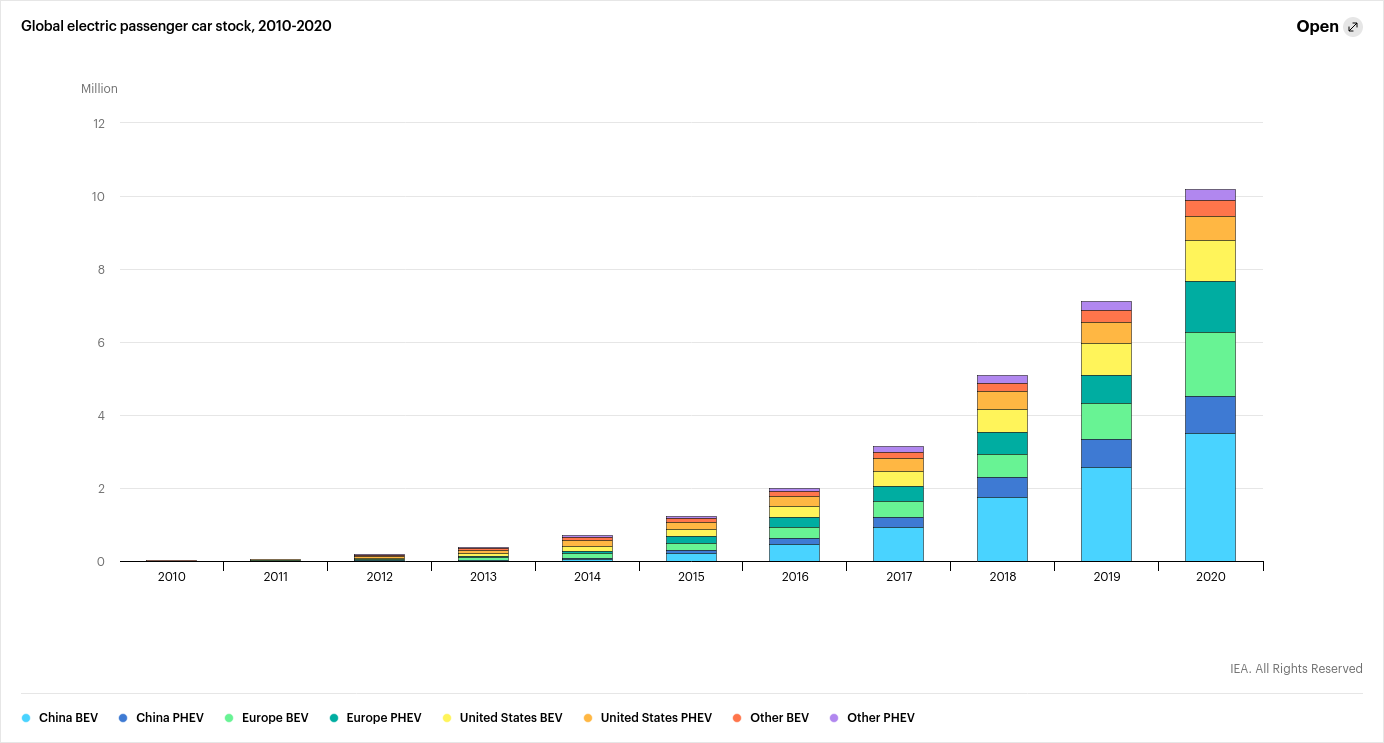

Trips in EVs getting easier is the trend, you should notice, and that is one thing that is dooming hydrogen cars. Not my perceptions or priorities. Why will governments and manufacturers continue to subsidize hydrogen cars?

Of course it got too easy, because the FC infrastructure got built, and except for Tesla all of it was built with government subsidies. Now, let's see you drive your e-Tron right now on I-80 between SLC and Cheyenne, or I-90 east of Missoula, or I-94 east of Billings, or I-25 north of . . .well, I could go on, but that poor horse is already dead. For that matter, let's remove all the DCFC stations that were built with government funds, or even just the EA ones (which is certainly government money), and see how well you can take a trip in your e-Tron. How does government-supplied infrastructure for BEVs somehow make it impossible to duplicate for FCEVs, when every government with a Hydrogen Strategy is subsidizing such infrastructure? From California's "2021 Annual Evaluation of Fuel Cell Electric Vehicle Deployment and Hydrogen Fuel Station Network Development", page 6:

LCFS HRI Program Update

The LCFS HRI program (and its parallel for DC Fast Charging of electric vehicles) was launched in

2019 with the intent to support ZEV infrastructure development. Prior to these additions, hydrogen

station operators were eligible to generate LCFS credits based on the amount of hydrogen sold

at their station(s). This presented a scenario with limited near-term potential to generate LCFS

credits, given the small number of FCEVs currently on the road. With the implementation of the HRI

provision, participating station operators are able to generate additional LCFS credits based on the

difference between station capacity and fuel sales. The net effect is that participating hydrogen

stations generate a total number of LCFS credits based on the station capacity. This is a constant

credit generation opportunity that significantly exceeds the expected near-term opportunity based

on fuel sales alone.Individual stations are subject to certain limitations that affect the maximum number of credits they

may generate through the HRI provision and stations are only eligible for these credits for a limited

period of 15 years. In addition, the total effect on the LCFS program is capped in order to ensure

the overall LCFS program can still deliver on its expected greenhouse gas reductions. The HRI

program thus far appears to be an effective tool to support the development of hydrogen stations

in California. There are also indications that the program has had a role in station developers being

able to develop larger stations, and more of them, than previously anticipated. Some new high-

capacity stations participating in the program have also reduced the price that customers pay at the

pump by approximately 20 percent.

OTOH, although we continue to subsidize them here in California (planning to build 200 H2 stations in state), surprisingly there are currently 23 stations either planned or in progress being built solely with private money (16 by First Element, and 7 by Iwatani). Please point to the number of DC FC stations in the U.S. that can say the same. As I previously mentioned, economies of scale have dropped the average grant per H2 station and per kg./day capacity considerably. Further from California's 2021 Annual report:

https://ww2.arb.ca.gov/sites/default/files/2021-09/2021_AB-8_FINAL.pdf Page 4.The announcement of awards in the CEC’s GFO-19-602 has fundamentally changed the outlook

of hydrogen fueling network development in California. The solicitation was the first in California

specifically designed to encourage the development of economies of scale in California’s hydrogen

fueling industry. The solicitation aimed to achieve this primarily through its structure that requested

applicants submit multi-year and multi-station plans. As reported in the 2020 Joint Agency Staff

Report on AB 8, the results of the solicitation appear to indicate that the solicitation was successful

is advancing economies of scale [14]. Figure 2 demonstrates how stations in GFO-19-602 are not only

larger than the previous solicitation (GFO-15-605), but the grant funding amount per station has also

decreased. Average grant funding amounts per kilogram/day of fueling capacity have dropped 65

percent between the last two solicitations. Stations awarded in GFO-15-605 received an average

grant award of $2,445 per kg/day fueling capacity; stations awarded in GFO-19-602 received an

average grant award of $847 per kg/day fueling capacity19.

Trips will remain easier in FCEVs (or ICEs) than BEVs given the same infrastructure because of their inherent capability, and will do so unless/until BEVs can achieve those same capabilities, or close enough that most people will accept the difference.

As far as road-tripping is concerned, our 2016 Toyota Mirai can only go where there are hydrogen filling stations. I recently described a clump of them in the LA basin and another cluster that serves the San Francisco area. There's also a lone station in a place called Coalinga that links these two regions, and another up near Donner Summit on the way to Lake Tahoe.

Turn back the clock to late 2012 and you'll see a map with just six Tesla Superchargers in more or less the same places. At the time, we marveled at how these revolutionary quick-charge stations would enable us to drive our newfangled 2013 Tesla Model S all the way to Lake Tahoe and back. Think of it!

You can see where this is going. Today's Hydrogen Highway is eerily similar to those early days of the Tesla Supercharger Network, and that realization recently prompted Jay Kavanagh and me to concoct a friendly contest. It's the 2016 Toyota Mirai versus the 2016 Tesla Model X, hydrogen versus electricity, fuel cell versus batteries. It's the Hydrogen Highway versus the Tesla Supercharger network.

Place your bets.

https://www.edmunds.com/toyota/mira...en-highway-vs-tesla-supercharger-network.html

I trust you remember which vehicle was faster on the return trip from SLT to Santa Monica, despite the much more limited infrastructure available to it that forced an initial detour 41 miles in the opposite direction then 100 miles on a heading about 70 degrees off the needed one, before finally heading towards the final destination? Just think what two (with a Mirai 2 or Nexo Blue, just 1) more H2 station(s) in the right place(s) would have achieved.

I've laid out what 'close enough' means for me and I suspect most potential BEV buyers, and we're still waiting to hear what you think it will take. I think the 500+ mile range Lucid Air (300 or so on trips when charging 20-80%, 300 miles in 20 min. charging) is pretty close, but until they can reduce the price by 75-80% (and offer a lot more types) it's not going to compete with ICEs, or FCEVs with appropriate infrastructure as above (still need 2/3rds price reduction to compare to a $50k Mirai 2) FTM. When they can combine the Lucid Air's range and charging speed (along with adequate longevity) with something like that below, that will probably do it:

. . . The company teased upcoming new electric vehicles including a Chevrolet small SUV that will cost around $30,000, as well as electric trucks from Chevrolet and GMC, crossover SUVs from Buick, and luxury vehicles from Cadillac. . . .

The $30,000 Chevy SUV should bring serious sales to GM because it's the size of the Equinox, GM's second-best-selling vehicle, President Mark Reuss said. He said the company is working on a smaller Chevy Blazer electric, as well as a smaller vehicle at a lower price point. He gave no details.

https://www.autoblog.com/2021/10/06/gm-revenue-ev-sales-investor-event/